Agentic Payments - When Software Gets a Wallet & a Will of Its Own

From recommendations to execution, AI enters the payment flow.

If you’re new here, Eximius is a pre-seed VC fund backing bold ideas across Consumer AI, FinTech, and Enterprise AI.

This week on Eximius Echo, we’re looking at a shift sitting at the intersection of all three: Agentic Payments.

For decades, the evolution of commerce has been a story of reducing friction. Cash gave way to cards. The internet birthed e-commerce. Smartphones put entire stores into our pockets. UPI made payments instant and habitual.

But through all these eras, one bottleneck remained constant: a human still had to click “buy.”

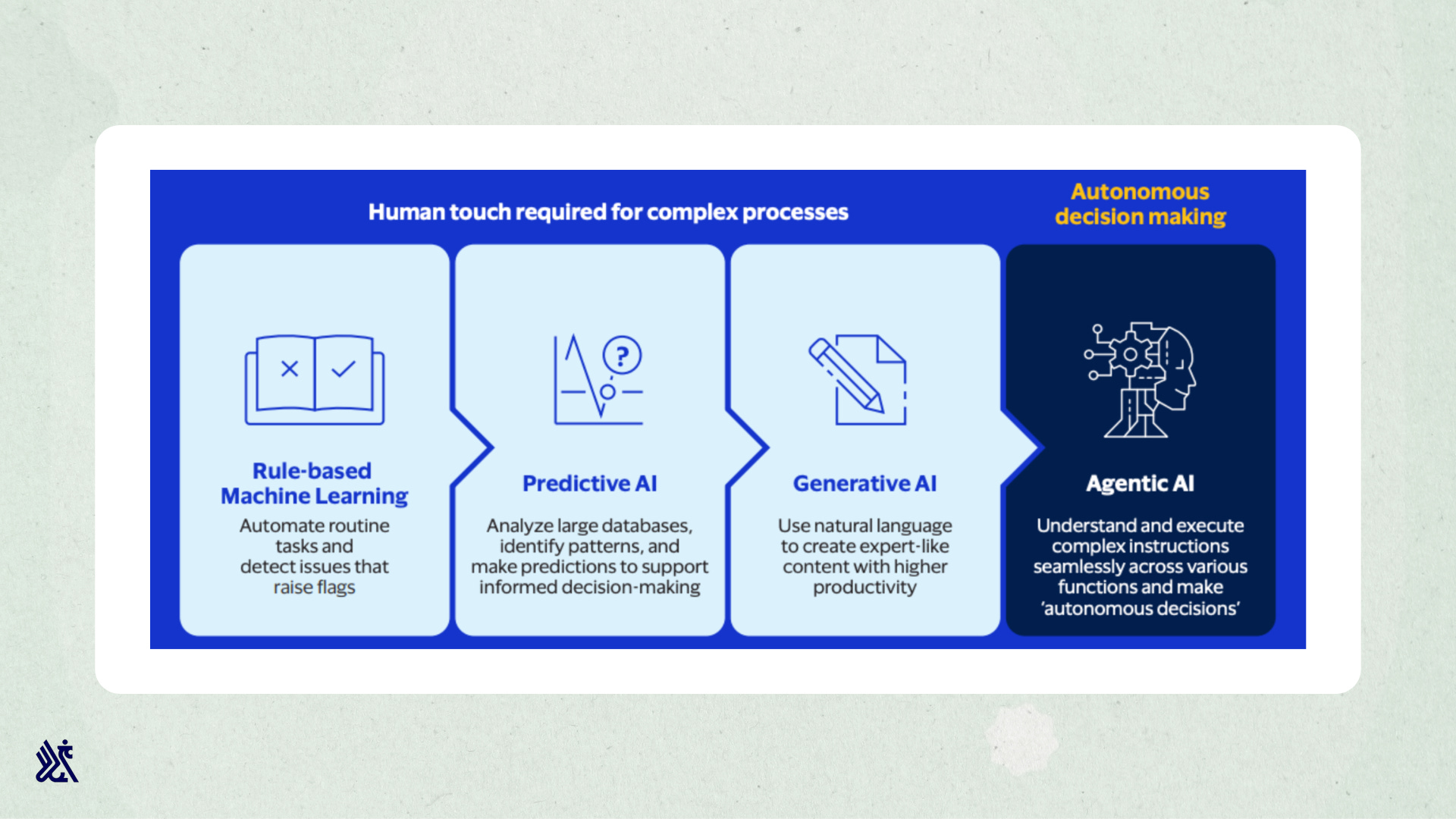

Today, we are entering the era of Agentic Commerce and Agentic Payments, where AI transitions from a passive assistant to an autonomous economic agent with its own wallet, permissions, and spending power.

This is the dawn of the “Do It For Me” economy.

The Engine Room: How Agentic Infrastructure Works

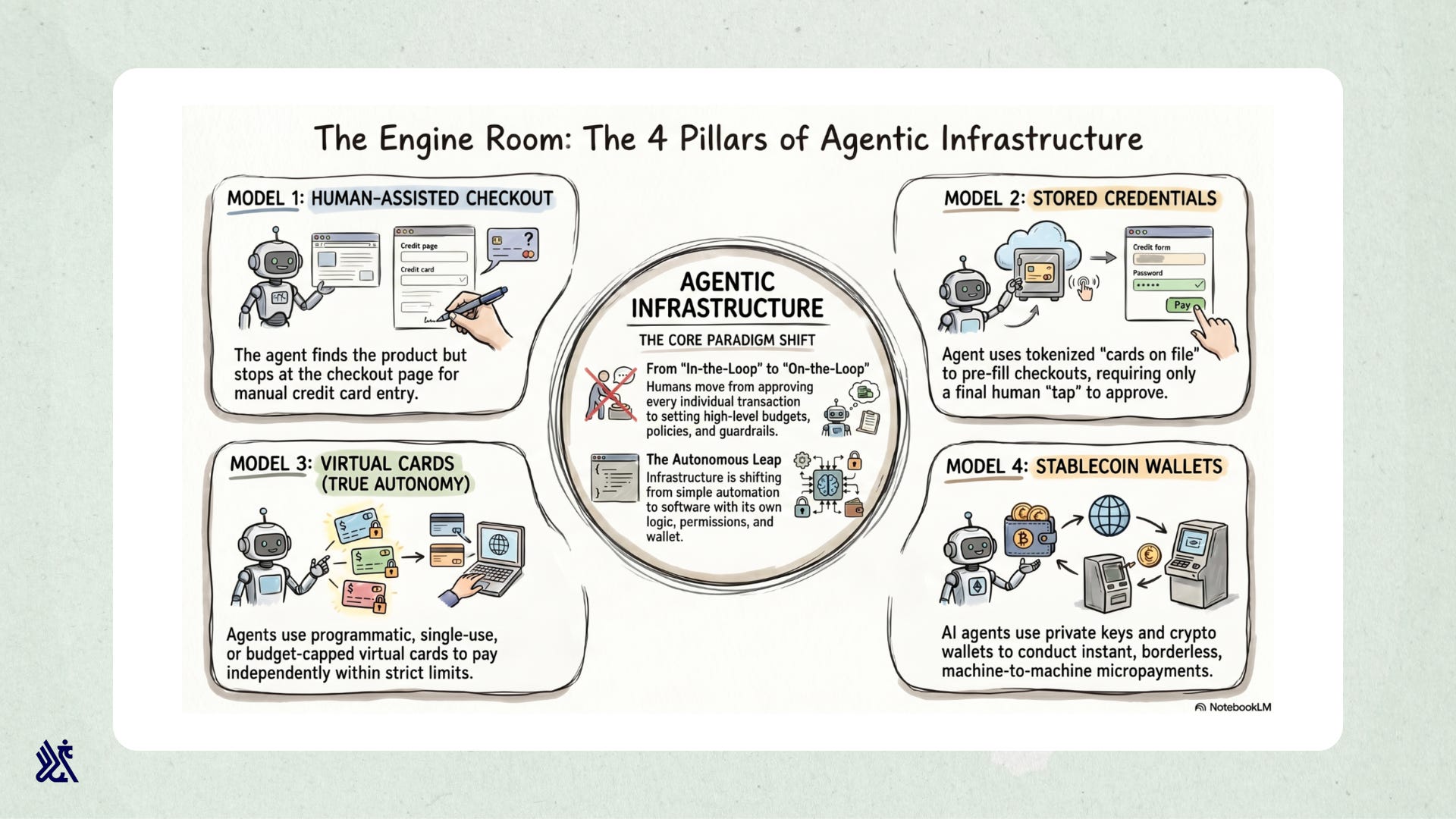

The core shift in agentic payments is moving from a “human-in-the-loop” model, where a person approves every step, to a “human-on-the-loop” model, where humans set the guardrails, budgets, and policies while AI handles routine decisions.

The infrastructure is evolving across four models:

Human-Assisted Checkout: The agent finds what you need, but stops at checkout for manual card entry.

Stored Credentials: The agent uses tokenised cards “on file” to pre-populate checkout pages, requiring a final tap of approval.

Virtual Cards: This is where autonomy begins. The agent is issued a single-use or budget-capped card with programmatic controls that allow it to pay within strict limits.

Stablecoin Wallets: The agent uses programmable wallets and stablecoins to conduct instant, borderless, machine-to-machine payments without traditional checkout flows.

Each model gives the agent more autonomy. The real unlock begins when payment authority becomes programmable, revocable, and auditable.

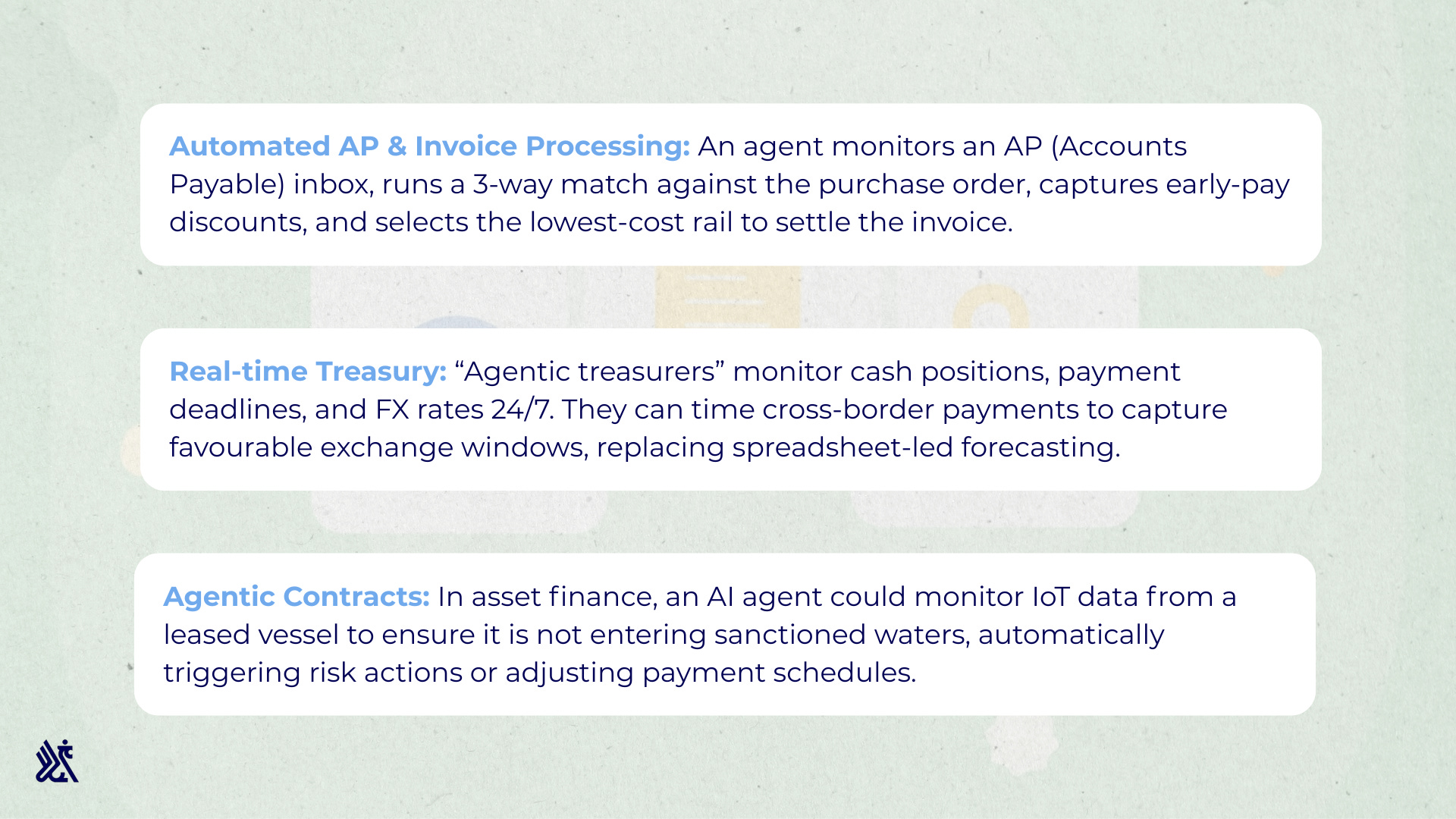

B2B Agentic Payments: Shifting from Hours to Outcomes

Traditionally, B2B payments operate like a slow relay race of initiation, approval, authentication, settlement, reconciliation, and reporting. Agentic AI collapses this into a closed loop in which payments are determined by context, policy, and real-time business conditions.

Some of the strongest use cases, with immediate ROI, are already clear:

The B2B bottleneck is data quality. If an agent operates on fragmented or dirty data, it will make poor financial decisions faster. Before enterprises automate payment execution, they need cleaner data architecture, stronger controls, and audit-ready workflows.

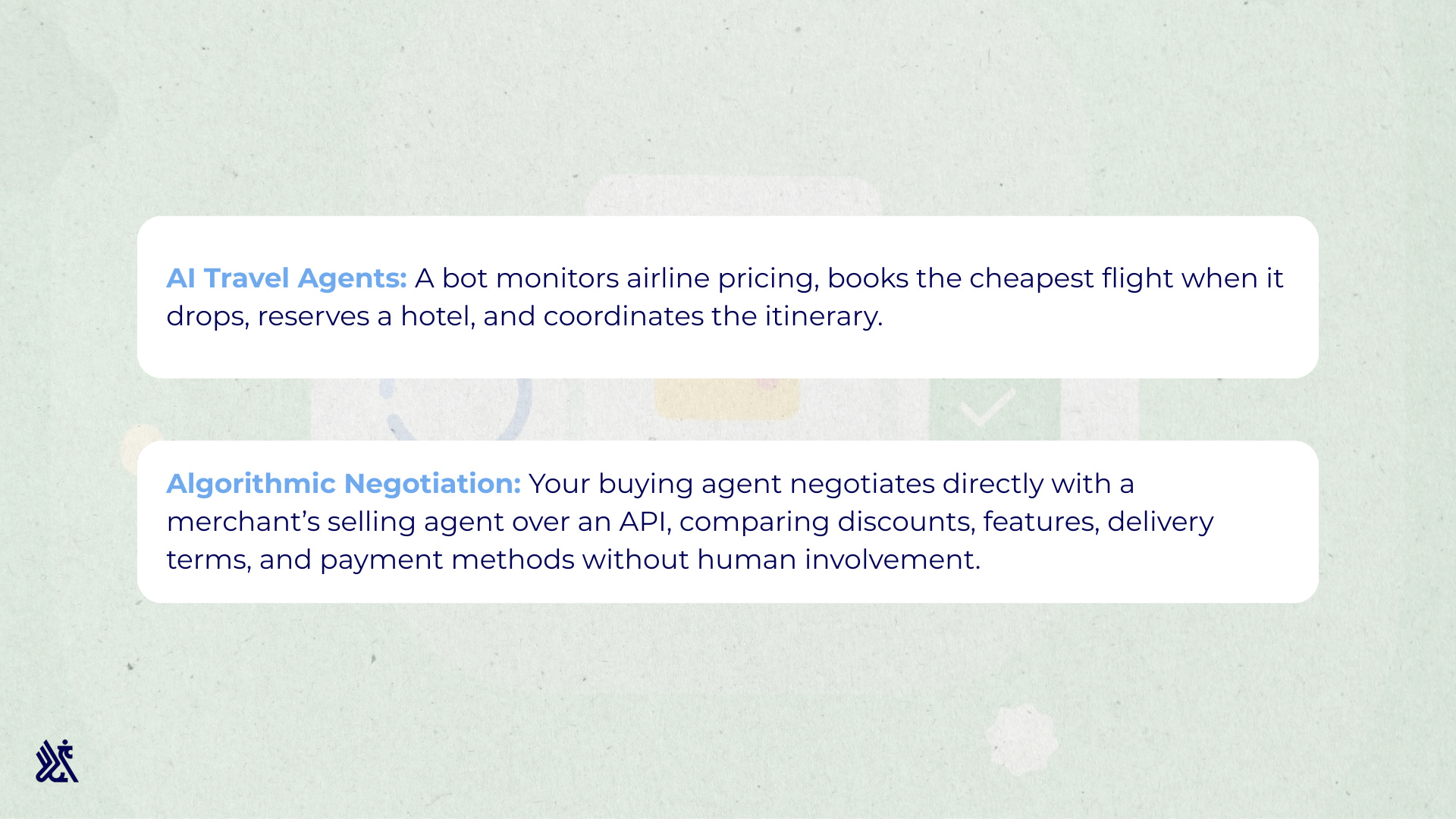

B2C Agentic Payments: The Rise of the AI Concierge

In the consumer space, agentic payments promise to reduce the friction of choice overload.

You set the parameters: a direct flight under a certain budget, an insurance renewal only if the premium drops, or a product purchase only during a sale. The agent handles discovery, comparison, timing, and payment.

Two use cases stand out:

But B2C has the harder trust problem. Merchants will need to decide whether to welcome AI shoppers, especially if agent-led purchases create higher returns, disputes, or chargebacks when consumers say, “I didn’t buy that, my agent did.”

Getting Platforms Agent-Ready

If an AI agent cannot see your products, read your terms, or verify your checkout, your business risks becoming invisible in the agentic economy.

Companies will need to prepare across four layers:

Expose Verifiable Surfaces: Catalogues, pricing, availability, return policies, and negotiation terms must become structured and machine-readable.

Audit the Handoffs: B2B companies need to identify human-dependent steps across procurement, payments, reconciliation, and approvals before handing agents payment authority.

Master Agent Marketing: Traditional marketing is built for human psychology. AI agents care about price, availability, trust signals, and policy fit. Brands will need to optimise for agents too.

Build the Trust Stack: Agent identity, scoped permissions, spend limits, anomaly triggers, and dispute-ready audit trails will become core infrastructure.

The Dark Side: Risks and the New Liability Fog

Giving software a wallet introduces a new class of risk, as follows:

Liability: If an agent buys the wrong inventory, overpays a vendor, or renews an unwanted subscription, who is responsible: the user, the developer, the merchant, or the payment network?

AI-Driven Fraud: Agentic AI could scale synthetic identity fraud, refund abuse, social engineering, and chargeback manipulation.

Frictionless Debt: If AI spends continuously in the background, the psychological “pain of paying” weakens. Consumers may lose visibility into subscriptions, renewals, and recurring obligations.

The industry will need new legal frameworks, agentic chargeback codes, Know Your Agent infrastructure, and cryptographically signed audit trails to prove when an agent acted within its mandate.

The Bottom Line

Agentic payments redefine who can participate in commerce.

The winners will be the financial institutions, merchants, and tech platforms that can verify AI agents, make their data machine-readable, and safely shift from manual workflows to autonomous execution.

Once software can act, it will need a wallet. And once it has a wallet, commerce changes.

If you’re building at the intersection of AI, payments, commerce infrastructure, or financial automation, write to us at pitches@eximiusvc.com. We’d love to hear what you’re building.

| A guest post by

|

Agentic commerce becoming frictionless is not the goal. Friction can be good for the consumer experience (The IKEA Effect)! Bertini et al. (2024) found that slowing down the purchase process actually improves customer satisfaction and loyalty long-term.

Bertini, M.Bertini, M., Aparicio, D., & Aydinli, A. (2024). Can friction improve your customers' experiences? MIT Sloan Management Review, 65(2), 42–47.

The point about data quality and controls stood out to me. In finance operations, faster execution only creates value when the underlying data, approval workflows, and audit trails are reliable. The opportunity is exciting, but trust and governance will ultimately determine adoption.