Demystifying the Quick Commerce Landscape in India

The demand is real. The scale is growing. But in quick commerce, category depth, execution, and retention will separate the noise from the winners.

Hi there!

This week on Eximius Echo, we deep dive into a category that’s moving fast - literally and figuratively. Quick Commerce has gone from a grocery convenience to a multi-vertical engine powering India’s next wave of consumer behaviour.

With 60% of buyers now expecting same-day delivery, and 1 in 3 wanting it in under two hours - Q-commerce isn’t just scaling, it’s evolving. From Fashion and Pharma to Baby-Care and BPC, the format is spreading wide. But the winners? They’ll be the ones who go deep.

In this edition, we unpack the metrics that matter, the players shaping each vertical, and where white spaces still lie wide open.

If you’re new here, Eximius is a pre-seed VC fund backing bold ideas in Fintech, AI/SaaS, and Consumer Tech. We use this newsletter to share insights, trends, and ideas from the sectors we’re passionate about. Let’s dive in.

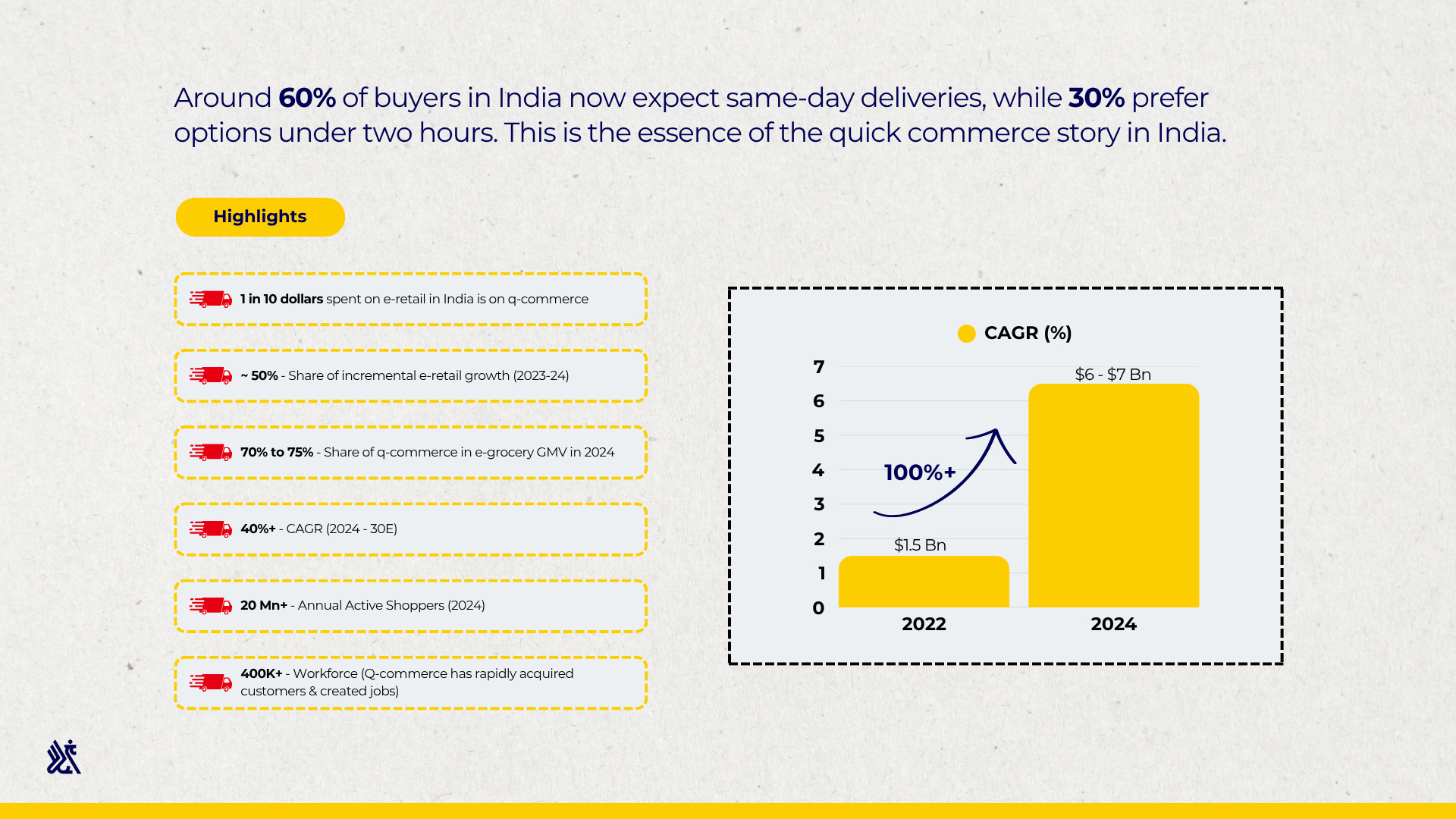

Around 60% of buyers in India now expect same-day deliveries, while 30% prefer options under two hours. This is the essence of the quick commerce story in India.

This raises an inquiry into whether people will pay to have something delivered in 15 minutes, instead of in a few hours or the next morning. While the normal presumption wouldn’t support this thesis, this is where stated and revealed preferences enter the picture. Validating the inherent demand for such solutions, the Indian consumers have surprised both investors and founders by adopting quick commerce at a particularly rapid pace.

Growing at a CAGR of 24%, quick commerce already represents 20% of the e-commerce market in India, and is expected to reach a gross order value of $35–40 billion by FY26. In addition to maturing customer preferences, this rise is also dominated by expansive investment from both new players as well as large incumbents such as Flipkart, Myntra, Amazon, etc. Major brands across the country are also looking to rapidly streamline their supply chains to calibrate them for quick commerce. Within FY25, just the top 6 FMCG brands in India (Hindustan Unilever, Britannia, AWL Agri Business) reported a combined INR Rs 4,400 crore in quick commerce sales.

Perhaps the most remarkable feature of quick commerce has been its versatility. While it commenced with a focus on groceries, 15%–20% of its GMV now comes from categories such as general merchandise, mobile phones, electronics, and apparel. Over the past year, we have seen innovative companies leveraging quick commerce across different vertical to elevate the customer experience. In this report, we will highlight the scope of quick commerce in India across these segments, and the nature of opportunities that still lie open. This leaves us with a very pertinent question on whether quick commerce is here to stay, and which categories are well poised to benefit.

Why Will Quick Commerce Work in a Vertical?

As highlighted above, quick commerce has percolated to a multitude of verticals across several industries with the demand being unprecedented.

As a result, we are frequently seeing founders wanting to leverage the frameworks of quick commerce in new domains and verticals. While the use cases for quick commerce are quite versatile, there are a few key features that industries need to possess to be ripe for quick commerce:

Large TAM: A large market size (offline and online) is a vital prerequisite to validate demand. Given that most quick commerce plays will only capture a share of the existing online market’s size initially, the category needs to have enough depth in terms of AOVs and volume in e-commerce, and a large offline presence as well to indicate future scalability.

Regularly Recurring Need: For the unit economics to be positive, customers must order the product/service at least once a week. Thus, the underlying need should be recurring with the repeat purchase of a few key items.

SKU Depth: To optimise for the AOV and the order frequency, the market should have a diverse catalogue of products to offer for immediate consumption.

Differentiated User Experience: Quick commerce platforms should also streamline key aspects of the user journey like product discovery, cart-building, etc. This will induce users to move away from horizontal plays and try new platforms.

While these factors greatly aid the onset of vertical commerce, the verdict is still not out in terms of where long-term winners will emerge.

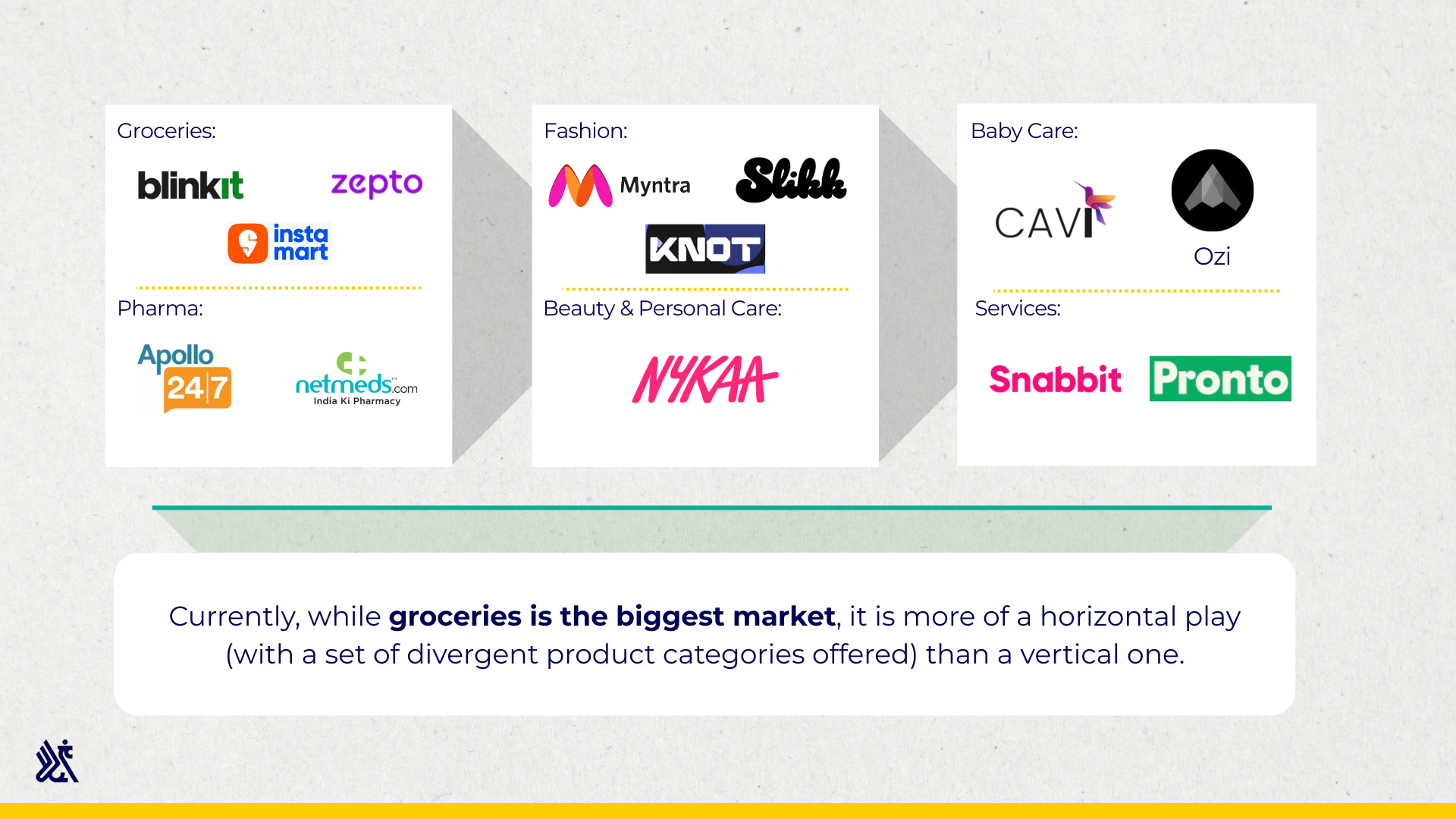

Currently, while groceries is the biggest market, it is more of a horizontal play (with a set of divergent product categories offered) than a vertical one. Therefore, there is considerable scope for new verticals to emerge by satisfying the above requirements and creating a differentiated experience. Below, we talk about the major verticals for e-commerce alongside groceries to highlight the nuances of each domain and the key considerations therein.

What Makes Every Vertical Tick

I. Groceries

Why does it suit quick commerce?

Market size: India's quick commerce sector contributed two-thirds of all e-grocery orders in 2024. Grocery also represents the largest segment for quick commerce with an 80-85% share.

Daily Requirement: Groceries are the biggest drivers of household spend in India. While urban households reserve 40% of their total outlay for groceries, rural households reserve ~50%. Thus, the propensity to order is quite high with a high number of orders per month.

Repeat Purchase of Key Items: Since grocery needs don’t diverge significantly for a person over a period, the platforms are able to manage their procurement better which enhances their margins and reduces spoilage.

Key Players

The market is dominated by three large players:

Blinkit

Revenue - $214 Million (Q4 FY25)

Orders per Day - 1.65-1.75 million orders in a day

AOV - INR 707

Number of Dark Stores - >1300

Number of SKUs - 5K-7K products.

Zepto

Revenue - $718 Million (FY24)

Orders per Day - 1.45-1.55 million orders in a day

AOV - INR 550

Number of Dark Stores - 1140

Number of SKUs - 13,000-14,000

Swiggy Instamart

Revenue - $86.1 Million (Q4 FY25)

Orders per Day - 1.05-1.15 million orders in a day

AOV - INR 499

Number of Dark Stores - >1200

Number of SKUs - >10,000

Key Considerations

Assortment: While only 18-20% of a platform’s partnered brands deliver ~80% of the revenue, it is important for players to optimize on variety and have a wide plethora of options to avoid the user turning to an alternative.

Pricing: As of June 2025, average discounts reached 20-25% of maximum retail prices, compared to less than 10% 2 years ago. Therefore, platforms need to have agile pricing modules to react to the competitors’ quotes as lower pricing is a significant reason for users moving to other platforms. Moreover, they also need to leverage these insights to shape their product mix for avoiding massive capital loss.

Inventory Management: Fresh fruits and vegetables form 60% of the total bills for a number of retailers in quick commerce. Therefore, companies must ensure that spoilage is at a minimum and their procurement is optimised to deliver quality products.

Pincode Serviceability: Deliverability is a key concern in this market. Platforms must identify their clusters well and optimise on their pincode serviceability to reduce the risk of prospective users churning.

II. Pharma

Why does it suit quick commerce?

TAM: Out of approximately 45,000 orders received daily on the Apollo 24/7 platform, 28-30% are fulfilled through its rapid delivery offering (under 20 mins). 90% are delivered on the same day. [Apollo 24/7 used as a proxy].

Recurring Need: 15-20% of the country’s yearly income is spent on medical expenses. Medicines and enhancement products are the biggest drivers of this spending which indicates a high re-order rate. The quick commerce orders for medicines are also usually for immediate consumption which boosts re-order rates.

No Discovery Necessity: Since orders are driven by the prescriptions from physicians, with little inclination from the patient for any alteration. Companies don’t need to aggressively push them, which reduces their expenditure on promotions.

Key Players

Apollo 247

Revenue - $33.5 Million (Q2 FY25) [Revenue from the digital pharmacy division]

Orders per Day - 45,000 orders per day

Net Meds

Revenue - $8.4 Million (FY24)

Key Considerations

Fulfilment Rate: Pharma is one of the most SKU sensitive categories as patient religiously stick to whatever medication is prescribed by their physician. Therefore, platforms need to have complete control over their procurement and inventory (usually via dark stores).

Discovery Effect: It is imperative for any player in this category to generate over INR 600 in AOV. This can only happen if the platform can successfully cross-sell and up-sell products to nudge the user to non-medicinal products.

Regulatory Concerns: Any platform needs to ensure that they have qualified people routinely checking the delivery packages and the inventory to ensure that there are no egregious deliveries, and verifying the prescriptions as well.

III. Fashion

Why does it suit quick commerce?

Market Size: Fashion contributes 3%–5% to the total non-food GMV for quick commerce. Myntra said nearly 50% of its total orders across 600+ Indian cities are now delivered within 48 hours through its M-Express service.

Recurring Need: An average Indian spends roughly $2500 per annum on just clothing. While also driven by the onset of new trends, clothing is inherently a recurring expense for Indian households.

Product Depth: The Indian fashion industry is home to a multitude of local and foreign brands, with over 22 billion garments produced annually in the country. Thus, customers have a wide variety of SKUs to choose from.

Key Players

Myntra

Revenue - $640 Million (FY24)

Orders per Day - 5,00,000 orders per day (From June 2023)

Slikk

Total Raise - $13.5 Million

Knot

Total Raise - $3 Million

Key Considerations

Return Rate: While the return rate in this category can go as high as 30-35%, maintaining it under 10% successfully is vital for any platform to succeed.

Average Cart Value: Platforms need to ensure that their AOV pegs closely to larger e-commerce platforms (~ INR 1500 for Myntra as an example) for optimal LTV.

Assortment: As mentioned above, a plethora of SKUs across categories is an inherent feature of the market, and a metric different platforms are benchmarked against each other at. Therefore, platforms should have a healthy catalogue of both domestic and foreign brands. Some even enter into exclusive partnerships with certain brands to enhance their appeal.

IV. Beauty and Personal Care

Why does it work for quick commerce?

Market Size: BPC contributes 3%–5% to the total non-food GMV for quick commerce. Quick commerce in the fashion and beauty space is likely to grow 40 to 45 percent in three years, and the beauty segment is experiencing 1.5 times high annual growth than personal care.

High AOV: The per capita spend on beauty in India is $22 and projected to reach $50 by 2030. This indicates the rising propensity to spend on BPC products, particularly on luxury products.

SKU Depth: 4 major segments of the market (skincare, makeup, fragrance, and haircare) are expected to showcase double-digit growth till 2028. This highlights the depth of the demand across different categories.

Key Players

Nykaa

Revenue - $994 million (FY24)

Yearly Orders - 54.5 Mn (From just the beauty vertical)

Key Considerations

Delivery Time: Nykaa dedicated 13% of its capex spend in H1FY25 just on acquiring warehouses to reduce fulfilment time. While the industry, as a whole, is new to quick delivery as even Nykaa has only started piloting 10-min delivery in select areas. New platforms can use this opportunity to create a clear differentiation on delivery time.

Repeat Volume: Brands should also aim to optimise on their repeat frequency to enhance their LTV for each customer. This can be done by adding new SKUs across categories, and creating gamified loyalty programs to boost user retention.

Daily Usage: It is preferable if the product mix offered by the platform caters to the daily use of the user to create a regular loop of using the platform to replenish their stock.

V. Baby Care

Why does it work for quick commerce?

Market Size: Online marketplaces saw a 34% increase in babycare purchases in FY24.

Massive Need: By estimates, approximately INR 11,50,000 is spent on a child’s care between the ages 0-3. This is spent on a diverse set of products from diapers, to beds, and even quilts. Thus, the market is quite deep with a multitude of lucrative subsegments.

Key Players

CAVI

Total Raise: $3M - $4M

Ozi

Total Raise: $3M - $4M

Key Considerations

SKU Selection: Identifying the right SKUs and suppliers is important to minimise the return rate, and optimise the repeat rate. Since this is a very quality-conscious segment, quality assurance needs to be thorough.

Discovery Effect: While durables represent only 12% of the spend share, they are high-value items. Therefore, platforms must gradually nudge users towards them for optimising the AOV.

VI. Services

Why does it work for quick commerce?

Market Size: The market for online, on-demand services is expected to reach USD 1.1 billion by 2030 with a CAGR of 22.3% from 2023-30.

Recurring Need: Households engage critical services like maids and cooks on a recurring basis. Thus, the risk of a user churning is quite low.

Diverse Offerings: The categories of services that a platform can deal in is quite diverse which amplifies the scope for cross-selling and up-selling.

Key Players

Snabbit

Total Raise: $25.5M

Pronto

Total Raise: $11M

Key Considerations

Booking Frequency: Ideally, platforms need to collect atleast one booker per person per week. However, they can also bill themselves as emergency services instead of recurring ones for a higher AOV, yet lower frequency (for example: helping a user book an emergency maid for a higher fare when their regular maid is unavailable).

Cross-selling: Since platforms deal in multiple services. They must also devise mechanisms to cross-promote different services during a session to optimise their LTV per client.

Conclusion

The Indian quick commerce landscape is turning out to be an exciting opportunity. Alongside favourably evolving customer habits, the mania of quick delivery has proliferated to a multitude of segments, all ripe for innovation. However, to succeed, brands need to maintain a disciplined vigil on a few key factors, all native to their respective segments.

In addition to a solid thesis, building in quick commerce demands a holistic team that can not only navigate the different challenges, but also successfully raise capital expeditiously to grow quickly and ward off competition.

If you are looking to build in this space, we would love to chat! Please reach out to us at pitches@eximiusvc.com.

| A guest post by

|