Growth of Alternative Investing in India

Alternative investments have rapidly gained traction in the global financial ecosystem over the last decade, forming a $20T industry that generates upwards of $200B in annual revenue.

Hi there!

This week on Eximius Echo, we dive into the rise of alternative investments, driven by an increase in disposable income across various income classes. As more individuals gain access to wealth and investment opportunities, there’s a growing interest in novel and non-traditional investment products. We'll explore how global trends are shaping this shift, how alternative investments have become a $20 trillion industry, and how sectors like real estate, private equity, and private credit are benefiting from this surge

If you’ve not heard of us, Eximius is a pre-seed stage VC fund focusing on fintech, AI/SaaS, frontier tech, and consumer tech. You can find out more here. This newsletter is an attempt to share ideas, insights, and context within the realms of our chosen sectors. Let’s dive in.

Global trends have shown an increase in disposable income across classes, leading to a higher investing propensity. The need for novel investment products, as a result, has seen a sharp rise over the last decade; and among the biggest gainers of this trend has been the asset class of alternative investments.

Alternative investments have rapidly gained traction in the global financial ecosystem over the last decade, forming a $20T industry that generates upwards of $200B in annual revenue. An agile financial ecosystem and the rising number of HNIs (globally defined to be people with over $1M in investable assets) globally have helped accelerate the adoption of alternative investments.

What is Alternative Investing - Global Trends and Trend-Setters?

‘Alternative investments’ is an umbrella-term, covering a wide range of investment options that go beyond the traditional modes - stocks, bonds, and cash. Examples of alternative investments include real estate, private equity, commodities, cryptocurrencies, etc.

These assets typically mature over a longer period of time and have a higher risk/reward profile in comparison to the traditional methods. Considering the nature of these investments, alternative investments have largely been structured around HNIs and other large investors - and this has been reflected across global trends, where the share of global financial wealth held by HNIs has grown from 41% in 2013 to 48% in 2023; a period where alternative investments have seen a 10X growth in AUM globally.

From an investor’s perspective, alternative investments have increasingly gained traction owing to its consistent returns over the market and increasing ease of investing. Private equity in the USA, for instance, has seen a 10 year annualised return of 15% - in comparison to traditional AMCs who’ve only had 7%. This benefit is not lost on HNIs, who have increased their wealth allocation for alternative investments to 15%, up 5% from what was seen a decade ago.

Industry reports show that more than half of the global HNI population has shifted towards using professional wealth management services. Traditional AIFs - venture capitals, hedge funds, and private equity - have reaped massive benefits from this wave, with AIF commitments growing at a rate of 54% annually over the last decade. The global market for alternative investment funds (AIFs) is expected to grow to $25.8T by 2032.

However, the growth of alternative investing has not merely been limited to equity funding. Private credit, for instance, has seen a significant surge over the last 5 years - 1.5-2X - with marquee investors such as KKR and The Carlyle Group now allocating over 40% of their portfolio mix towards private credit.

Similarly, the push to make alternative investing more accessible to groups beyond HNIs and corporates has seen the exponential rise of start-ups emerging through the gaps left by these traditional players to offer further alternative investment opportunities. Since the start of 2021, alternative investment start-ups have raised upwards of $18.2B in funding globally, with some key companies leading the charge.

● Immutable (Australia) - Provides blockchain-based infrastructure for NFT games and applications, and has raised $857M in funding from investors including Temasek.

● Micro Connect (Hong Kong) - An online investment platform for micro and small businesses. Micro Connect has raised $578M so far from investors such as Sequoia China and Goldman Sachs.

● Roofstock (United States) - Roofstock is an online platform for real estate investments, and has raised $373M in funding from investors such as SoftBank and Lightspeed.

While crypto-currency, NFT, and fantasy sports have emerged as the major winners among start-ups owing to their more mass-oriented nature, real-estate investing and crowd-funding have also emerged as strong contenders as alternative investments gain further traction globally.

The Indian Story

Alternative investments collectively hold over 20% of the overall global AUM today, and this number is projected to grow exponentially with previously under-penetrated markets such as the Middle East and South East Asia seeing a rise in HNI wealth. These regions house the fastest growing HNI populations globally, and will play a key part in the growth of alternative investing. India has emerged among the frontrunners in the adoption of alternative investments, with the country’s share of Asia-Pacific private equity and venture capital investments rising to ~20% in 2024.

India currently has an AUM of $400B in alternative investments, with the number projected to grow 5-fold to reach $2T in the next decade. This is in line with the projected growth of HNIs and UHNIs in the country, with numbers expected to breach 19,000 UHNIs and 16 lakh HNIs by 2027, alongside a rise in disposable income across classes among the country’s population.

AIF schemes in India have seen a surge from 600 in 2020 to upwards of 1300 in 2024 - with Category II AIFs leading the way in this growth. India’s start-up revolution has been a major growth driver, with the country now housing the world’s third largest start-up ecosystem with over 1.5 lakh start-ups officially recognised by DPIIT, thus allowing further inflow of funds across sectors through AIFs. Real estate has emerged as the leader within alternative investments, with the first nine months of FY25 seeing the real estate sector raising INR 28,560 Cr through private equity investments. Real estate has accounted for 17% of total alternative investments this year.

As has been seen with global trends, India’s alternative investing journey has not just been limited to HNIs, and instead has been pushed towards the mass-affluents and other rungs of the investing spectrum - thereby increasing the value flowing into the segment.

Companies such as Jar, Deserve, and Strata have paved the way for alternative investments to be brought beyond the cream of Indian investors, with the space seeing over 650 companies coming up in the last 5 years and receiving over $300M in funding in this period. Some of the major business models that have come up in this space include:

● Jar - A platform for small-ticket automated savings and gold investment. Jar has raised $56M in funding so far, and reported revenues of $6.8M in FY24.

● PropertyShare - A real estate investment trust platform that enables individuals to invest in pre-leased commercial properties in India. PropertyShare has raised $52M in funding so far, and reported revenues of $5.4M in FY24.

● Dezerv - Wealth management service provider that offers personalized investment solutions to individuals. Dezerv has secured $60M in funding, and reported revenues of $3.1M in FY24.

● Stable Money - Fixed income investment platform for individuals, now also offering government bonds, corporate bonds, and credit cards against FD. Stable Money has raised $25.3M in funding, with reported revenues of $477K in FY24.

A key contrast between Indian companies coming into the alternate investing space versus global trends has been the high number of real estate-focused players in the Indian ecosystem - PropertyShare, Micro Mitti, hBits, Strata, etc.; especially with a rise in companies providing fractional ownership in real estate. Players such as Guardian Link and MetaSpace have tried to mimic leading global segments such as NFTs to little success, with the Indian audience at this point seemingly content with savings and real-estate based platforms, while the likes of Infinyte Club and LetsVenture provide HNIs with private investment opportunities.

Headwinds and White Spaces in the Indian context

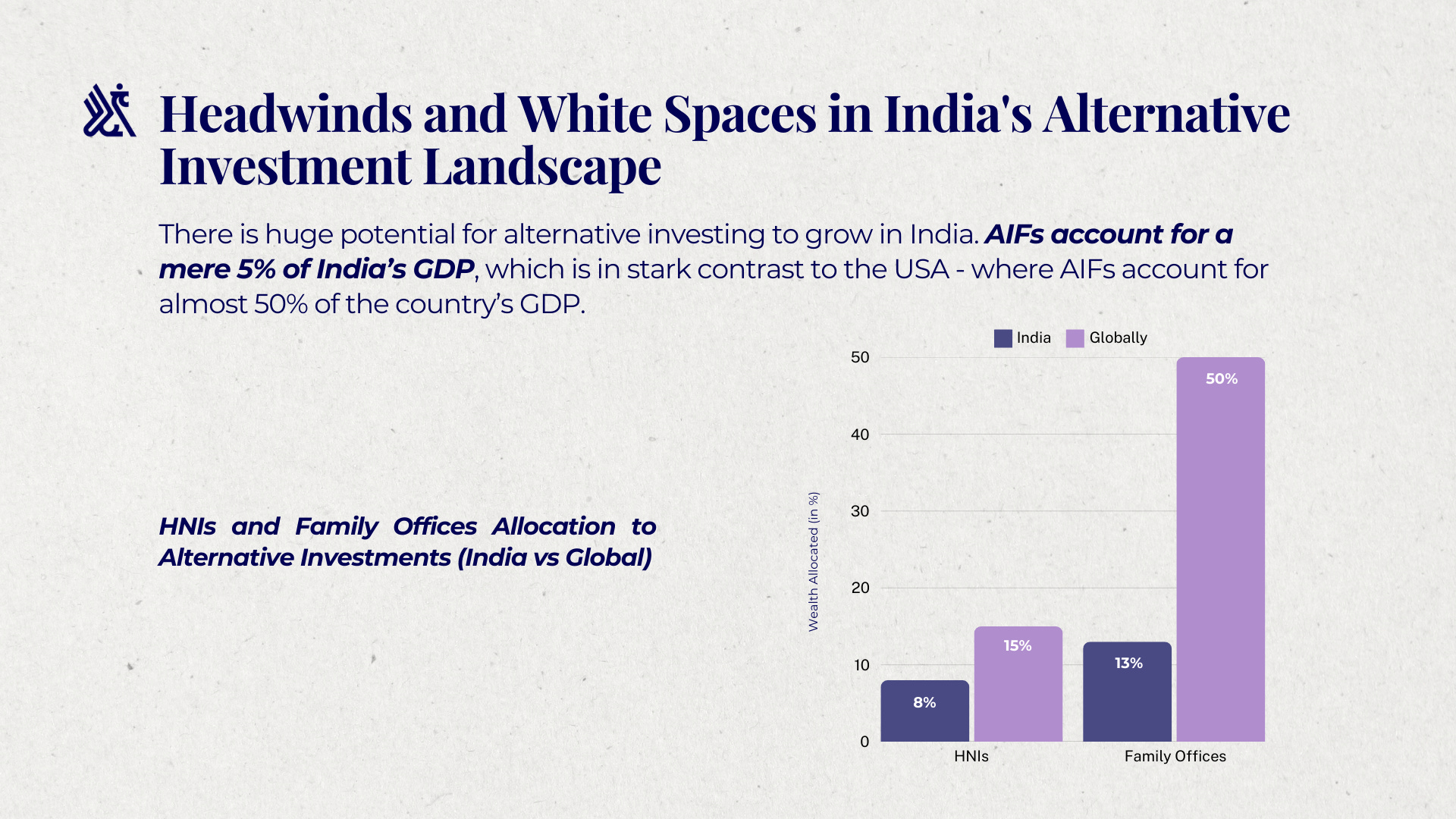

While the tailwinds - micro and macro - are for all to see in terms of growing investment affinity across all classes of the society, and increasing income levels, there is huge potential for alternative investing to grow in India. Case in point - AIFs account for a mere 5% of India’s GDP, which is in stark contrast to the USA - where AIFs account for almost 50% of the country’s GDP.

India continues to remain under-penetrated in this segment, as showcased by 2 major groups of investors - HNIs and family offices. HNIs in India allocate 7-8% of their overall wealth towards alternative investments, which is less than half of what global HNIs do. Similarly, while family offices globally allocate over 50% of their funds to alternatives, Indian family offices only allocate 13% of their funds to alternatives, with this number projected to grow to 18% by 2027.

This can, in some part, be attributed to the relative slowdown in investing across the private markets, where there has been a shift in preference towards mature business models as opposed to the 2021-22 period of taking higher risks. This is shown by funding trends, with PE-VC funding into the market reducing by 63% in FY23 in comparison to FY22, and declined further by 49% in FY24. Late-stage deals accounted for 39% of total private equity deal value in FY24.

However, a large part of the puzzle remains the vast white-spaces - which could further open up avenues for alternative investing in the country.

● Private Credit - Global trends have moved towards private credit now being a big part of the equation, and India has seen a similar rise too - growing from $0.7B in 2010 to now being at over $18B. However, with projected requirements of $70-80B of private credit by 2027, there remains huge potential for growth in this space.

● Special Situation Funds - Distressed debt funds and special situation funds have created a niche in the global markets - specially the more developed ones - but are still in the nascent stage in India. Individual global funds often manage assets in the range of $5-12B, whereas leading Indian SSFs manage assets around $2.4B.

● Climate and Deep Tech investments - Currently, less than 5% of VC funding goes into deep tech, and while Green bonds and ESG funds exist, climate-focused investments remain at a very nascent stage in India. Deep Tech and Climate Tech have fueled the next set of investments globally, and one can expect this to be a space India focuses on - especially with ambitious government targets around carbon neutrality and additional support being provided for tech-led innovations within the country.

Conclusion

In conclusion, alternative investments as a segment has been making the right noises - both globally as well as in India. With regulatory support and increasing awareness, we should expect to see this growth trajectory further continuing as more white spaces start being covered and market adoption increases along the next stage of growth for this industry.

If you are looking to build in any space within fintech, AI/SaaS, frontier tech, and consumer tech, please reach out to us at pitches@eximiusvc.com.

| A guest post by

|